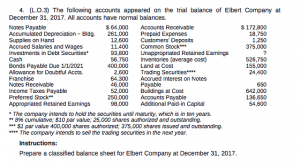

Any irregularities discovered during this stage must be investigated and corrected to maintain the integrity of financial records. By routinely reconciling accounts, businesses also safeguard against fraud, avoid financial mismanagement, and align their accounting records with legal and tax requirements. Reconciling bookkeeping accounts is a fundamental activity in managing a business’s finances. It involves verifying that the amounts recorded in the company’s books match the corresponding financial transactions. This process is crucial to ensure the venture debt 101 accuracy of financial statements, which are relied upon for decision-making, reporting, and compliance. Through account reconciliation, discrepancies can be identified and rectified promptly, reducing the risk of financial errors that may lead to misstated information.

However, generally accepted accounting principles (GAAP) require double-entry bookkeeping—where a transaction is entered into the general ledger in two places. When a business makes a sale, it debits either cash or accounts receivable on the balance sheet and credits sales revenue on the income statement. Keeping accurate financial statements is the easiest way to simplify your bank reconciliation process. FreshBooks accounting software helps you track income and expenses and generate reports and financial statements. Try FreshBooks for free to streamline your tax preparation and bank reconciliations today.

After scrutinizing the account, the accountant detects an accounting error that omitted a zero when recording entries. Rectifying the error brings the current revenue to $90 million, which is relatively close to the projection. Michelle Payne has 15 years of experience as a Certified Public Accountant with a strong background in audit, tax, and consulting services. She has more than five years of experience working with non-profit organizations in a finance capacity. Upgrading to a paid membership gives you access to our extensive collection of plug-and-play Templates designed to power your performance—as well as CFI’s full course catalog and accredited Certification Programs. So, thoroughly checking the capabilities of the AI solutions you shortlist is crucial.

Q5. What is bookkeeping reconciliation?

This document summarizes banking and business activity, reconciling an entity’s bank account with its financial records. Bank reconciliation statements confirm that payments have been processed and cash collections have been deposited into a bank account. The reconciliation process involves comparing internal financial records with external documents to identify and correct discrepancies. This includes investigating any differences, accrued vs deferred revenue making necessary adjustments, and documenting the process for accuracy. Finally, the reconciliation is reviewed and approved to ensure the financial records are accurate and complete.

What is the reconciliation process?

Similarly, if there are deposits appearing in manufacturing cost the bank statement but are not in the cash book, add the entries to the cash book balance. It involves calling up the account detail in the statements and reviewing the appropriateness of each transaction. The documentation method determines if the amount captured in the account matches the actual amount spent by the company.

- Accounting for these delays is key to reconciling the total amounts on the company’s financial statement and the bank statement.

- The reconciliation statement thus is essential for identifying discrepancies between the two records.

- The documentation method determines if the amount captured in the account matches the actual amount spent by the company.

- For lawyers, account reconciliation is particularly important when it comes to trust accounts.

- For law firms, for example, one key type of business reconciliation is three-way reconciliation for trust accounts.

What is a three-way reconciliation in accounting?

Human error in the data entry process can sometimes lead to incorrect amounts or miscalculations on a business’s financial statements. While it cannot entirely erase the potential for data processing errors, using accounting software can reduce the likelihood of errors to help generate more accurate financial statements. Take note that you may need to keep an eye out for transactions that may not match immediately between the sets of records for which you may need to make adjustments due to timing differences. For example, a transaction that may not yet have cleared the trust bank account could be recorded in the client ledger, but may not yet be visible on the trust account bank statement. The accounting team in an organization is responsible for reconciling accounts at the end of each financial period to ensure that the GL balance is complete and accurate.

Bank Reconciliation Process Flow

The process is used to find out if the discrepancy is due to a balance sheet error or theft. Accuracy and completeness are the two most important things when reconciling accounts. Companies usually perform monthly or quarterly reconciliations to have accurate financial records at the end of the year.

In order to perform reconciliations accurately, accountants need to have all the relevant documents including bank statements and vendor information. In accounting, the term reconciliation specifically refers to the comparison of two sets of financial records. During an account reconciliation process, a company compares its financial records with external documents. Companies use this process to prevent fraud, ensure their records are consistent, and stay compliant. Within the balance sheet, equity accounts represent the shareholders’ stake in the company.

Leave a Reply